author

Carlos Balthazar Summ

author

Carlos Balthazar Summ

post date

10/02/2025

reading time

6 minutes

share

The multifamily market in the United States is known for its adaptability and strong demand. This type of property consists of buildings or residential complexes intended exclusively for rental, catering to those who prefer renting over homeownership.

In 2024, the segment remained strong and demonstrated significant resilience, with a record number of new constructions since the 1980s and high demand, almost as intense as in the years immediately following the pandemic. Despite this, rental prices saw only a slight increase of just 0.3%, while occupancy levels remained stable, with approximately 94.4% of units rented. Here in Brazil, this market segment is still in its early stages but is gaining traction as more people and investors recognize its potential. This presents an opportunity to learn from successful models abroad and adapt them to our local reality.

Some examples of companies operating under this model in Brazil include Greystar, which runs the Ayra development, the housing-as-a-service startup Yuca, and Share Student Living— an investment of one of our funds — among others.

For 2025, rental prices are expected to show positive growth, while vacancy rates will slightly increase overall, with some markets being exceptions to this trend. Property values remain under pressure due to persistently high and volatile interest rates, while the financial performance of these assets continues to be moderate.

From a geographical perspective, regions such as the Sun Belt and Mountain West lead in new supply, accompanied by high demand. Developments in these areas are expected to benefit from inflationary pressures, resulting in higher rental values.

Despite signs of slowing down, the U.S. economy remains solid, with GDP growth, moderate inflation, and a stable labor market at full employment. However, the possibility of a recession in 2025 remains under evaluation due to the risks posed by excessively high interest rates and the potential resurgence of inflation.

Even though interest rates remain high and volatile, capitalization rates remain stable and below the historical average. Despite uncertainties, market experts believe that multifamily asset values are likely to continue increasing.

Miami: A city with significant appreciation in multifamily property prices between 2020-2024 (image: Canva)

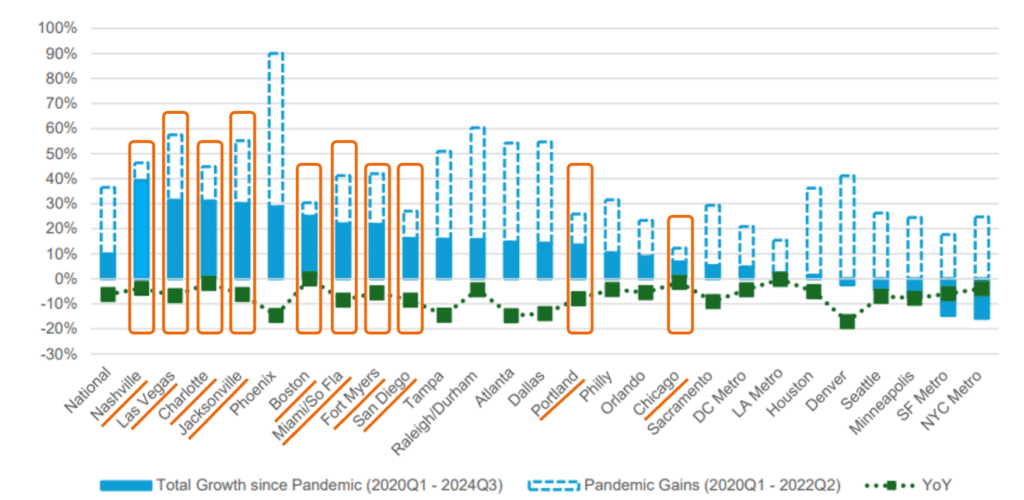

Cities such as Miami, Nashville, Las Vegas, Charlotte, Boston, Fort Myers, Portland, Jacksonville, San Diego, and Chicago have managed to keep up—albeit at a slightly slower pace—with the record appreciation observed during the pandemic period (Q1 2020 – Q2 2022). These cities are among those that have shown solid growth over the entire 2020-2024 period.

Source: Freddie Mac, Real Capital Analytics CPPI

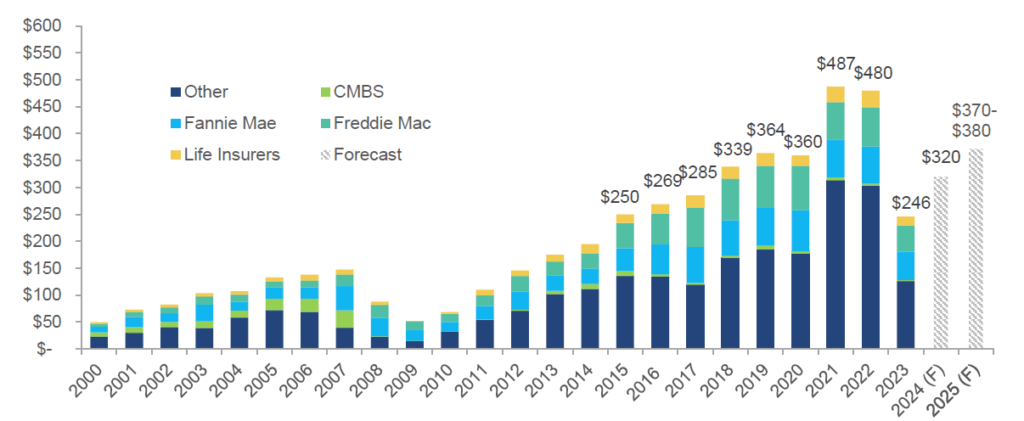

Multifamily transactions in the first quarter of 2024 were relatively moderate but gained momentum in the second and third quarters due to declining interest rates.

For 2025, the total transaction volume in the multifamily sector is expected to reach between $370 billion and $380 billion.

This projected growth is attributed to several factors, including:

• A backlog of transactions that were postponed while interest rates remained high.

• The need to refinance loans that cannot be extended.

• The stabilization of property prices and capitalization rates.

These factors reflect a gradual recovery in the multifamily market this year.

New Purchases and Multifamily Property Guarantee Volume (in billions of dollars)

Source: Mortgage Bankers Association, ACLI, Wells Fargo, Intex Solutions Inc., Freddie Mac projections

Note: 2024 and 2025 data by Freddie Mac as of November 2024.

Supporting this outlook is a report published by Bloomberg on January 17: “U.S. Housing Starts Top All Forecasts on Multifamily Construction” by Michael Sasso.

The article states that residential construction in the U.S. accelerated in December to the fastest pace since early 2024, driven by a surge in multifamily projects and a more modest increase in single-family homes. According to government data, new residential constructions increased by nearly 16%, reaching an annualized rate of 1.50 million units, recovering after three months of decline. This figure exceeded all estimates in a Bloomberg survey of economists.

In comparison, single-family home projects, which account for the majority of new housing construction, rose by 3.3%, reaching an annualized rate of 1.05 million units—the highest level since February 2024. Meanwhile, the construction of new multifamily projects, such as apartment buildings, skyrocketed by almost 62%.

The report also highlights that, despite the strong monthly growth, new home construction throughout 2024 was the slowest since 2019. Mortgage rates remained above 6% for the entire year and are now above 7%, exacerbating the affordability crisis initially triggered by record-high home prices.

The economy is following a “soft landing” trajectory—a strategy used by central banks to slow economic growth in a controlled manner to avoid a recession. The Federal Reserve continues to achieve full employment and price stability, although recession risks persist.

Even with this stable economic scenario, the multifamily market in 2025 is expected to see rental income growth, with occupancy rates remaining below historical averages.

However, the strong demand seen in 2024 is expected to continue into 2025, which is crucial given the peak supply anticipated during this period. Elevated supply will remain the main challenge in the short term but is expected to return to pre-pandemic levels by 2026. Therefore, despite short-term obstacles, the multifamily market is well-positioned for continued growth, supported by housing shortages, high costs in the homeownership market, and favorable demographic trends that drive demand for rental housing.

In the United States, we have been investing in multifamily properties since 2017, when we began the development of Terraces @nomad in New York. This project consists of 49 rental apartments, including 15 units designated for low- and moderate-income tenants, particularly teachers, firefighters, police officers, and other essential city workers.

In Miami, we have acquired over 350 workforce housing units from Resia, the American subsidiary of MRV. From this portfolio, we have already divested approximately 150 units, selling them at an opportune market moment and delivering solid returns to investors.

For 2025, we are developing a 300-unit project near Brickell, featuring a rooftop leisure area with a swimming pool, private lounges, a gym, and a linear park with a pet-friendly space.

author

share

CIX Capital is an investment by Maiz: maiz.com.br