author

Gabriel Piccoli e Lígia Carvalho

author

Gabriel Piccoli e Lígia Carvalho

post date

18/03/2025

reading time

7 minutes

share

In 2020 and 2021, the Covid-19 pandemic led countries to implement isolation policies and to restrict activities, forcing the closure of in-person services. Companies adopted remote work models to stay operational, with employees working directly from their homes.

Today, that reality seems like a distant past, as more and more companies return to in-person office spaces. In the US, President Donald Trump revoked remote work for federal government employees, and companies—especially in the technology sector—are increasingly reinstating the requirement for full-time, in-person work.

The American office market has been showing signs of recovery in what appears to be a solidified trend. In this article, CIX Capital analyzes the key factors driving this comeback.

The isolation policies and the widespread shift to remote work directly impacted the dynamics of the office sector in the United States, starting with occupancy rates:

Source: CoStar

At the beginning of 2020, occupancy stood at 91%. However, following the pandemic’s impact in the first quarter, a sharp decline began, continuing throughout the period and closing the fourth quarter of 2024 at 86%, a 5% drop.

A segment that has long been the cornerstone of commercial real estate portfolios, offices also experienced a significant decline in sales volume compared to pre-pandemic levels.

Regarding in-person work, sentiment among major corporate leaders is mixed: some are adopting a hybrid model to avoid the high costs of office rents and general property maintenance expenses, while others believe a full return to in-person work is the path forward.

Source: CoStar

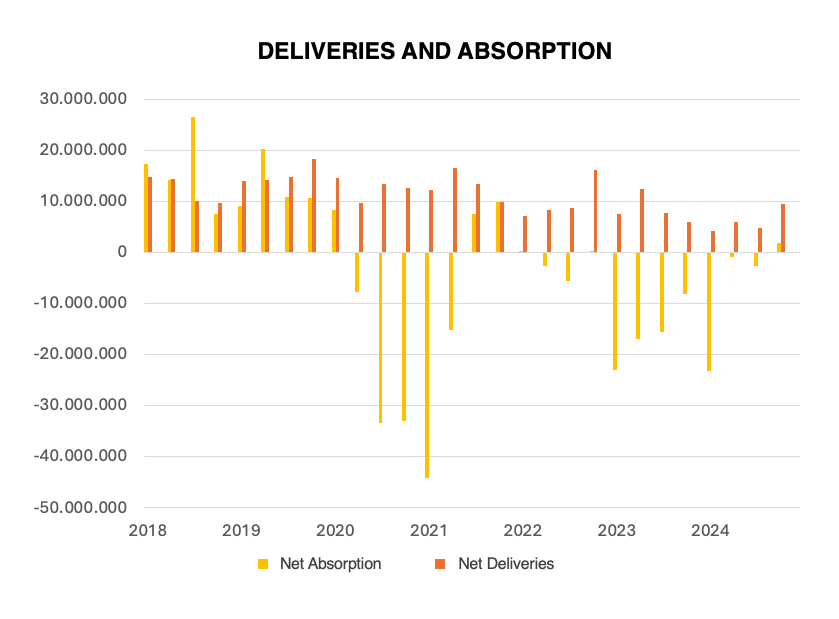

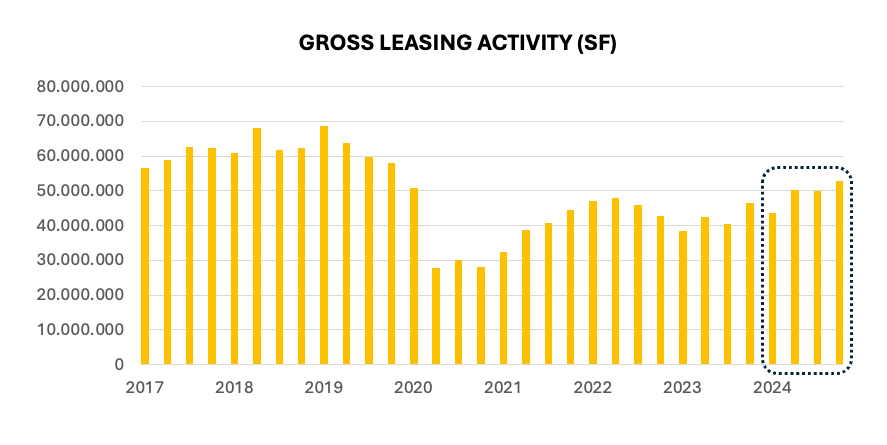

The close of 2024 marked a significant milestone in the recovery of the US office market. With leasing activity gaining momentum throughout the year, the fourth quarter recorded the first positive net absorption since Q4 2021—a period when the market saw a temporary boost likely driven by partial returns to the office, incentives, contract renegotiations, and workspace reconfigurations by companies.

Gross Leasing Activity (GLA, in square feet) reached post-pandemic highs for three consecutive quarters, with the fourth-quarter volume representing more than 92% of pre-pandemic averages.

Source: JLL

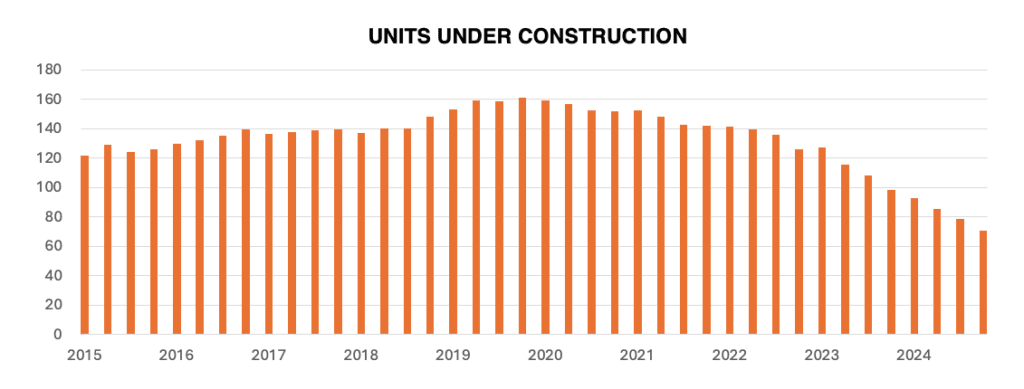

With many companies requiring a more regular in-office presence in recent years, the number of requests for reductions in leased space has dropped significantly.

Landlords, in turn, are seeing a moderation in requests for concessions and discounts, which have surged in recent years. They are expected to experience greater relief in the medium term, as the development pipeline has shrunk drastically compared to 2019 levels, and underperforming properties are being quickly removed from the market for conversions and repositioning projects—such as the so-called retrofits.

Source: JLL

The labor market is less robust compared to recent years but remains resilient. For instance, office-using industries created 763,000 new jobs in 2023 and 615,000 new jobs throughout 2024.

Payrolls in key sectors grew by just 0.5% over the past year, but strong growth of over 4% in outpatient healthcare services boosted demand within the medical office sub-sector.

Tenants remain active but cautious: More lease agreements were signed in 2024 than was typical in the 2010s; however, these deals were 15 to 20% smaller than pre-pandemic averages. Smaller tenants continue upgrading their spaces, while larger occupiers tend to stay put—helped by slower headcount growth and limited by the increasing scarcity of large spaces in premium buildings.

Market Context

Demand for office space has begun to show signs of recovery, with leasing volume in the US growing 11.5% year-over-year in the third quarter of 2024, according to CBRE Group. However, vacancy rates remain high, reaching 19% nationwide and up to 37% in markets like San Francisco.

Refinancing challenges are also significant, with $300 billion in office-related debt maturing in the coming year.

Additionally, 2024 saw a resurgence in transactions, with sales volumes increasing by 17% compared to 2023, according to MSCI Inc. As reported by Bloomberg, notable deals—from sales of stakes in trophy properties to distressed asset acquisitions—reflect evolving owner strategies to navigate this challenging environment:

Key Transactions:

● 980 Madison Ave., New York — $560 million

RFR Holding sold the Manhattan building for $560 million to Bloomberg Philanthropies.

● One Vanderbilt, New York — 11% Stake Valued at $4.7 Billion

SL Green Realty sold an 11% stake in the prestigious Manhattan tower to Japan’s Mori Building Co.

● Pacific Corporate Towers, California — Debt Converted to Equity

Beacon Capital Partners and 3Edgewood acquired a majority stake in the property’s $485 million senior loan at a 60% discount.

● 701 Brickell, Miami — $443 million

Elliott Investment Management purchased the office tower from Nuveen Real Estate, marking the second-largest office sale in Florida’s history.

● 5 Times Square, New York — Debt Converted to Equity

Apollo Global Management converted mezzanine debt into equity ownership in the renovated office building.

The US office market is set for a decisive shift in 2025, with stabilization paving the way for a new cycle. As office attendance reaches a steady level and the economy heads toward a soft landing, occupiers are expected to plan their portfolios with greater confidence.

Source: CBRE

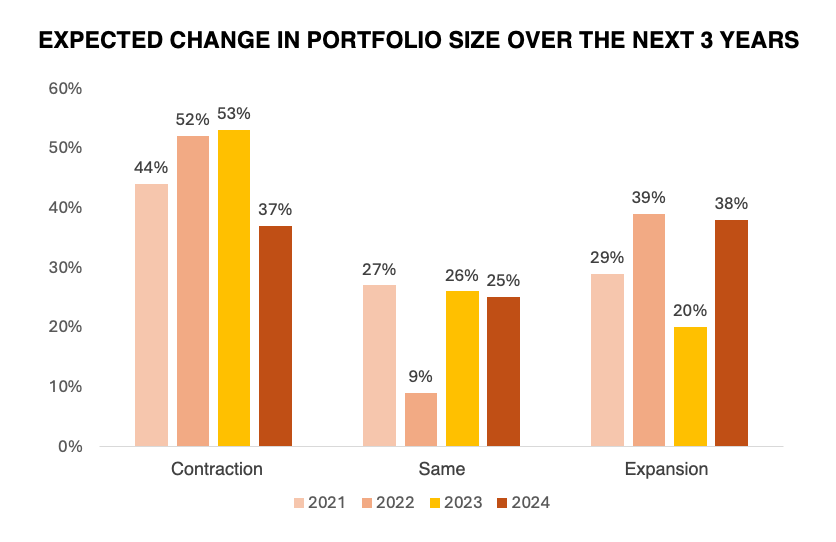

More than 38% of respondents in CBRE’s 2024 Occupier Sentiment Survey plan to expand their portfolio needs over the next two years, while 25% expect no change. This is expected to support positive office space absorption in 2025.

Based on the chart, we observe a shift in occupiers’ intentions: moving from expectations of space contraction to maintaining—and even expanding—leased areas, which favors the absorption of office space.

The “rightsizing” process—adjusting space—should continue in 2025 due to pre-pandemic inefficiencies and the reduction of space driven by hybrid work models. However, much of this adjustment has already occurred over the past four years.

Positive changes, combined with a significant slowdown in new supply and falling interest rates, create the most optimistic scenario the market has seen in years. However, some challenges remain, such as slower-than-expected growth in office-using jobs, a large amount of sublease space available, and high vacancy rates in less desirable properties.

The increase in demand for office space is expected to result in a 5% rise in leasing volume in 2025. Smaller occupiers seeking between 10,000 and 20,000 square feet (1,000 to 2,000 m²) will account for more than half of total leasing volume.

Amid this office market recovery, one standout is the strong growth of over 4% in outpatient healthcare services, which continues to drive demand for the medical office building (MOB) sub-sector.

CIX Capital has been investing in MOBs across the US since 2019 through the CIX Flagler Healthcare Fund, a fund with a portfolio of 11 assets located in states such as Florida, Texas, Nevada, Oklahoma, and California.

author

Gabriel Piccoli e Lígia Carvalho

share

CIX Capital is an investment by Maiz: maiz.com.br